SurplusInterconnectionin Ohio

Accelerating Clean Energy Deployment by Leveraging Existing Grid Infrastructure

Ohio's clean energy transition faces critical interconnection bottlenecks despite significant grid infrastructure

The Problem

Data Center Demand Surge

Ohio is the 4th-largest US data center market with 12.3 GW of BNEF-tracked IT capacity, 9.8 GW of which is still pre-construction. Hyperscalers have committed multi-billion-dollar campuses around New Albany and Licking County: Amazon $20B+, Google $6.7B, Meta $1.5B Prometheus 1 GW AI campus, and Microsoft $1B (paused). Extended interconnection timelines limit Ohio's competitiveness for these high-value projects.

Gridlock in Interconnection Queues

Ohio has 41.3 GW (nameplate) across 226 active projects in the PJM interconnection queue, the third-largest state queue in PJM. Connection timelines exceed 5 years, plus another 2+ years for construction.

Skyrocketing Capacity Prices

PJM capacity prices in the AEP Ohio zone surged from $28.92/MW-day (2024/25) to $269.92/MW-day (2025/26), a ~9x increase, and the 2027/28 BRA cleared at the $333.44/MW-day price cap with a 6,623 MW shortfall, signaling urgent capacity need.

Gas Plant Supply Chain Constraints

New gas plants ordered today won't come online until 2030-2031 at earliest, with capital costs surging to $2,200-2,800/kW for recent combined-cycle projects (GridLab, 2025).

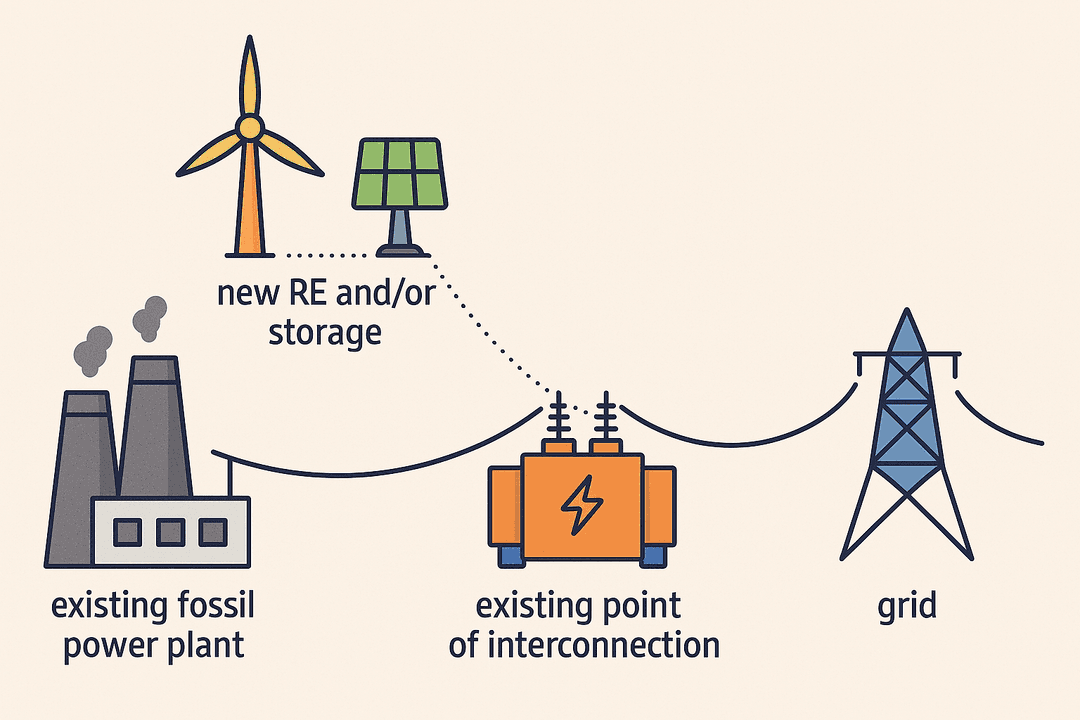

The Solution: Surplus Interconnection

Surplus Interconnection for Ohio

Surplus Interconnection Service allows new electricity supply resources to connect to the grid using existing infrastructure that serves already operating generators, without exceeding the total output capacity already allocated to the existing resource. FERC Order 845 (2018) cleared a regulatory pathway for generators to add new electricity resources to the grid by utilizing surplus capacity at existing interconnection points.

Key Results

Available Surplus Capacity

Ohio can add 21 GW of clean energy capacity through surplus interconnection: 10.6 GW solar + 6.5 GW wind + 4.2 GW storage. This includes 8.3 GW at thermal plants and 13.1 GW at existing renewable plants—all at existing sites without new transmission.

Cost Savings

Surplus interconnection can save $1.8 billion in interconnection costs by leveraging existing infrastructure, equivalent to $367 per Ohio household. This conservative estimate only accounts for interconnection savings—additional benefits from co-location and transmission utilization would increase total savings significantly.

Fast Deployment

Surplus interconnection projects can be completed in 12-18 months compared to 6+ years for standard queue projects. PJM and MISO's surplus processes follow streamlined study approaches, enabling rapid deployment when no network upgrades are triggered.

Thermal Interconnections

Ohio has significant thermal capacity, with plants operating at less than 15% capacity factor (mostly gas peakers), leaving grid connections idle most of the time. By 2030, building new solar will be cheaper than operating existing thermal plants. By co-locating solar and wind at these sites, we can bypass lengthy interconnection queues and deploy clean energy using existing infrastructure.

Key Results

Abundant Local Resources

~300 GW PotentialApproximately 300 GW of combined solar (268 GW) and wind (32 GW) potential exists within 6 miles of Ohio's thermal plants. This local resource is more than ten times current state demand and can be deployed at existing interconnection points.

Urban Area Plants

1 Plant ExcludedPlants with more than 30% urban land within their interconnection buffer are excluded from the surplus interconnection analysis. In Ohio, this affects 1 plant — West 41st Street (32 MW gas peaker in Cleveland) — which remains a good candidate for battery storage once it retires.

Economic Crossover

7.6 GW by 2030By 2030, building new solar will be cheaper than operating 7.6 GW (29%) of Ohio's existing thermal capacity on an unsubsidized LCOE basis. Surplus interconnection captures this opportunity at existing sites without queue delays.

Ready for Renewables

8.3 GW by 20308.3 GW of renewable energy (6.4 GW solar and 1.8 GW wind) can be economically integrated at Ohio thermal plants by 2030.

Quick Wins Available

5.0 GW Ready5.0 GW of Ohio thermal capacity operates at less than 15% capacity factor, leaving grid connections unused most of the time and creating immediate opportunities for surplus interconnection.

Renewable Interconnections

Ohio's existing renewable capacity operates at low capacity factors—meaning interconnection capacity sits idle most of the time. Adding battery storage can enable additional renewable capacity and dramatically increase capacity factors, effectively turning variable renewables into firm power resources.

Key Results

Massive Renewable Potential

143 GW TotalOhio's existing renewable sites have substantial potential for additional capacity, with approximately 128 GW of solar and 15 GW of wind resource potential within 6 miles of existing RE plants.

Significant Storage Potential

4.2 GW StorageAdding 6-hour battery storage at Ohio's solar and wind sites would deliver 4.2 GW (25 GWh) of firm, dispatchable capacity — helping meet peak demand and enhance grid reliability.

Expanded Renewable Capacity

8.9 GW CombinedOhio's existing renewable interconnections can support an additional 4.2 GW of solar and 4.7 GW of wind, more than tripling current renewable nameplate capacity (213% increase) with no new grid connections.

Maximized Utilization

81% Solar & WindDeploying RE and storage at existing interconnections maximizes expensive grid infrastructure usage in Ohio, lifting interconnection utilization from 18% to 81% for solar and from 29% to 81% for wind. This transforms intermittent renewables into firm resources comparable to gas CCGT plants.